Any country that wants to prosper financially must set up solid economic and monetary policies. These policies will become structures to ensure the smooth running of the economy.

A similar idea happens in crypto. To make a project successful, it needs a good plan for how its tokens will work to keep it afloat. Any project with bad tokenomics will sink.

What is tokenomics?

Tokenomics is the concept behind how the law of demand and supply plays out in crypto and NFT. It emerged from two words: token and economics.

A token is a unit of an asset on the blockchain. It can exist in the form of a fungible or non-fungible token. Economics studies scarcity, consumer behavior, and efficient use of resources.

The key difference between traditional economics and tokenomics is how the latter is spelled out in code.

Key features of tokenomics

The tokenomics of any crypto or NFT project should address some key features. Here are a few of them:

1. Minting. The Central Banks create money through "minting" in the traditional banking system. Hence, new notes of a dollar or any currency are called "new mints." Similarly, protocols also mint new tokens on the blockchain. The main question is, "How can the tokens be minted and remain valuable?"

This is where the concept of supply comes into play. Tokenomics revolves around maximizing the potential of a crypto token through the law of demand and supply. Some projects have an unlimited token minting term but checkmate the surplus with other measures. In contrast, some mint a maximum amount per time and gradually release them into their ecosystem.

2. Utility. Utility refers to the benefits a token offers to the token holders. How does it add value? What do people stand to gain by holding the token? That is the utility. The utility is an important factor to consider when analyzing crypto tokenomics. For example, an utility of MATIC is how Polygon users can pay transaction fees with it.

The utility can also exist in the form of access. For instance, holding 400 CODE tokens gives anyone access to become a member of Developer DAO. If the token has nothing to offer, it might not fly. Or even if it does, it will fall flat shortly. At the same time, utility is relative as it means different things to different people.

3. Distribution. Distribution deals with the rationale behind how a token is issued and allocated. Projects often have categories of token holders, either the core team or the general public. Meanwhile, the mode of launch is a huge factor in distribution. This depends on whether the team wants to raise some funds with the tokens or launch immediately.

In cases where they need to gather funds, they often do pre-sale. In token pre-sale, the team distributes some percentage of the token to early investors before it goes public. But there would be no early token distribution if they were to launch immediately, otherwise called a fair launch. All the distributions will be after they have gone public.

4. Vesting and Release. A token could have been distributed yet unreleased. Some projects adopt the vesting term in their smart contracts. Vesting is a practice where allocated tokens cannot be immediately available. Instead, they will be released gradually over some time. Vested tokens are often allocated to the core team or early-stage members. The plan can be to release 7% of the tokens every 2 months. The main idea is so the core team will not suddenly dump their tokens.

5. Token Burns. The value of a thing goes up when it is scarce. This is the rationale behind burns in crypto. The community might do it when they notice an excessive total circulating supply. In practice, the core team burns some tokens by sending them to an address no one can access.

By doing so, those tokens will forever be ejected out of circulation. For example, Solana carries out an ongoing token-burning mechanism. It burns 50% of each transaction fee. Others, like BNB, burn periodically. Note that token burn is not an essential utility. It is only a control mechanism.

6. Incentivization Models. Incentivization models are more relevant to blockchains and DeFi protocols. Any protocol that will thrive for long must have an established method of rewarding those at the core of its tokenomics. Who are those behind how the token is created? If they are not properly compensated, the structure of the crypto tokenomics will fall face-flat.

How blockchains approach incentivization often depends on their consensus mechanisms. For instance, Bitcoin utilizes the proof-of-work mechanism. It incentivizes its miners by giving them some cuts from the gas fees. Ethereum, a PoS-based blockchain, rewards its validators for their stakings. Incentivization works quite differently with DeFi protocols. Protocols such as UniSwap offer liquidity provision programs. They reward their liquidity providers with yields.

However, protocols should focus on creating tangible values that attract users instead of enticing them with undue incentivization.

7. Inflationary and Deflationary Models. Tokenomics designers have two major approaches to follow. These are inflationary and deflationary models. The main goal of the deflationary tokenomics model is to ensure a limited total amount in circulation concerning its price. Burning mechanisms are the lifeblood of maintaining deflationary tokenomics.

The first method of burning is to burn some percentage on each transaction. This is how Solana operates. The second method is for the team to burn the tokens at appointed periods. The inflationary model increases the number of tokens circulating over time. It does not place a stringent capitalization on token minting.

Polkadot and Ethereum are two popular examples of blockchains using the inflationary approach. There are various ways a protocol can introduce inflationary tokens. They can either mint on demand or with a schedule. The inflationary model requires caution. The tokenomics designers must ensure availability does not lead to market surplus and lower token value.

This is why some protocols have a hybrid of both inflationary and deflationary models. It is even better for robust adaptability in more diverse market conditions.

Tokenomics Analysis

Profitable crypto traders should be able to analyze the project's tokenomics. How can the general tokenomics features be merged to assess a project's token? As mentioned earlier, tokenomics rest on the law of demand and supply.

Beyond the surface level, there is more to tokenomics analysis. Here is a brief insight into token supply.

Token Supply Mechanisms

Unavailable tokens cannot be analyzed. This is why token supply is the first precursor of tokenomics. Token supply appears in different forms, and here are some of them:

- Maximum Token Supply. A token's maximum supply refers to how many exact amounts can be minted. Will the maximum token supply remain the same after token burns? No. Calculate the difference between the total token supply and burned tokens to know the new maximum supply of a token. For instance, if the total token supply is fixed at 10, 10 is the maximum supply. But when 2 out of the 10 tokens are burned, the new maximum supply reduces to 8. Avalanche is one of the projects with a maximum supply. It has a maximum supply of 720,000,000 AVAX.

- Circulating Supply. Circulating is straightforward. It is the number of tokens available in the market at a particular time. Of course, circulating supply does not mean total supply. By implication, circulating supply does not include vested, reserved, or burned tokens. It only deals with the available amounts at a time. Even though Uniswap has a 1,000,000,000 total supply, only 753,766,667 are in circulation.

- Total Supply. The total supply is the total amount of tokens a protocol created, whether or not they are in circulation. It applies more to projects with fixed tokenomics. By logic, burned tokens are no longer part of the total supply. According to Coingecko, DOT of Polkadot has a total supply of 1,287,574,631.

- Initial Supply. Initial supply is the total amount of tokens circulating when the secondary listing is approved. The usual pathway of token adoption is for primary and secondary exchanges to list them. Initial supply only starts to count when secondary exchanges list the token.

- Unlimited Supply. Unlimited supply is another unique method of token supply. It has no limit to the number of mintable tokens. Some predefined conditions have been met, and the token supply will keep increasing. A good example of a token with an unlimited supply is Ethereum. So far, validators stake their ETH and will keep earning new ETH in return. This increases the supply over time.

- Market Capitalization. Investors would always want to know how much a particular project is worth. The project's tokenomics indicate this as the market cap. The market cap of a token is the product of the circulating supply with the current market price. For instance, if a token has a circulating supply of 10 and trades at $3 per token. Then the market cap is $30 (3 x 10 = 30). Using TRON as an example, it has a circulating supply of 91,460,369,850 with a price of 0.069. So its market cap is $6,353,962,248.

- Fully Diluted Valuation. An FDV is similar to the market cap, but they are different. While the market cap is for the current circulating tokens, FDV deals with the maximum ones. If token A has a maximum supply of 15 and trades at $3. Its FDV will be $45.

Token Demand Mechanisms

A token's supply system is not the only reason to bag it. It must be balanced with a corresponding token demand mechanism. If the demand mechanisms are faulty, the tokenomics will crumble with time. The hard question of token demand is, "What realistic reasons would people want to part with their funds in exchange for the token?"

- Game Theory. It is an economic principle about how people make rational choices based on the benefits they will get from something. Game theory explains the market demand around any token. Yield farming and staking are two different elements of game theory in the blockchain space. A trader can lock up their crypto asset to get rewards. The longer the lock-up, the greater their gains.

Some platforms support either farming or staking, while some support both. For instance, Binance users can stake BNB to get more BNB in return. But protocols like PancakeSwap provide more protocol revenues. First, the users can lock up or farm two token pairs to get CAKE. They can still stake the same CAKE to earn more cake. - Communal Vibrancy. Even though a token is doing well in terms of game theory, the vibrancy of its community is equally important. How many people also believe in this project and are willing to ride with it?

Check public opinions to answer these questions. How active is the community on Discord and Twitter? Are they working on any real-life innovations? The more active the community, the higher the token can perform on the chart.

The simple logic behind communal vibrancy is to check if everyone else finds the token worthy of purchase. If people would not buy it because they do not believe in it, its fall is imminent.

Factors Which Make Tokenomics Bad

Although a project can fail for many reasons, bad tokenomics is a major pointer. Certain factors make up bad tokenomics. Once these factors are in a project, they are potential red flags. Here are 3 of them:

- Massive Pump and Dumps. Projects often draw market attention with token pre-sales. But massive allocation to early investors gives them more power, which can be dangerous. They can later pump and dump the token on the new investors. Examine an equitable distribution before bagging into any project.

- Unlimited Supply. Unlimited supply is not a bad implementation in itself. For instance, Ethereum has an unlimited supply. But it is understandable because it solves a lot of problems. So it will always have market relevance. However, choosing an unlimited supply without a convincing reason can be a bad tokenomics factor. The founding team can choose this model for suspicious reasons. Once the token has more market value, they can mint more and cash out the liquidity.

- No Actual Utility. Every project must have a real-time utility token. A utility token must have some purposes it serves within the ecosystem. USDC and USDT are examples of tokens with actual utilities. They serve as modes of payment and stable investments. Once there is no tangible reason for people to buy crypto, its market value will eventually crash. This applies more to meme tokens.

Tokenomics Examples

It is time to consider some examples for a real-time overview.

1. AVAX

Avalanche is a layer-1 blockchain network that was launched in 2020. It uses the proof-of-stake consensus mechanism and boasts close to 1,000 validators. AVAX is the native and governance token of Avalanche.

Utility. AVAX has two major utilities. It serves as:

- Unit of account within Avalanche subnets and a

- Medium of paying transaction fees

Incentives. Validators can earn up to 11% APY when they stake AVAX.

Supply. Although it has a maximum supply of 720,000,000 AVAX, only 324,781,476 circulates. All the vested AVAX would have been released by 2030.

Distribution. 50% of the tokens are directed towards staking rewards. The remaining 50% is partitioned among community efforts, public sales, and airdrops.

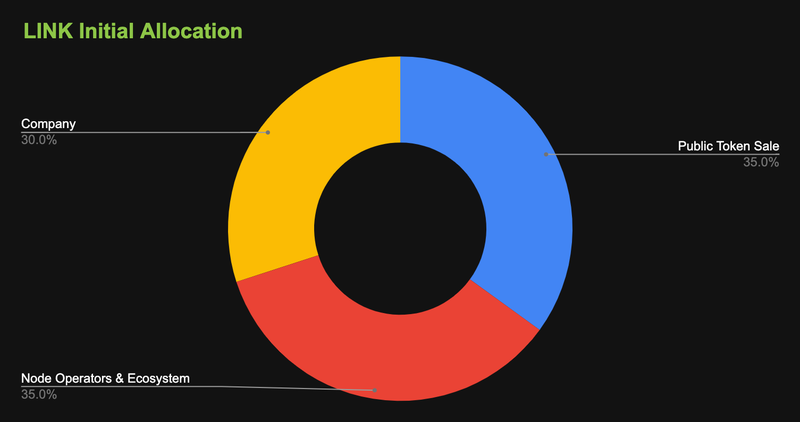

2. LINK

It is the native token of Chainlink, a decentralized oracle in Web3.

Utility. Its main use case is for development purposes. Developers pay with LINK to tap into the oracle infrastructure of Chainlink.

Incentives. Chainlink incentivizes its stakers by giving them around some percentage of tokens.

Supply. It has a maximum and total supply of 1,000,000,000 LINK. But only 491,599,971 LINK are in circulation at the moment. It has a regular supply of 250,000,000 LINK over time.

Distribution. Moving on to its distribution, it has an initial distribution in this proportion:

- Public token - 35%

- Ecosystem - 35%

- Company - 30%

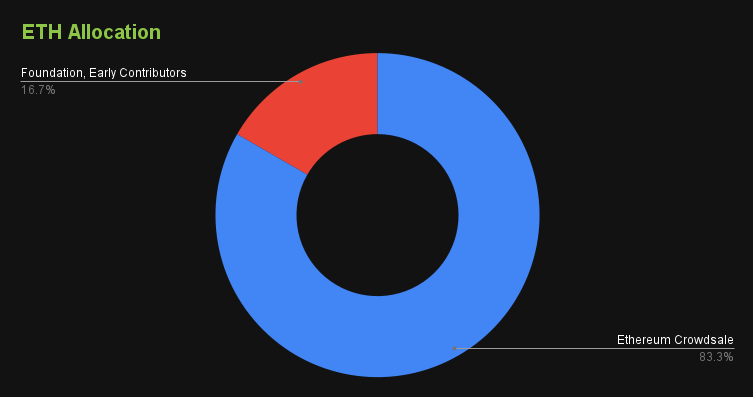

3. Ether

It was one of the earliest blockchains after Bitcoin. As a major L1, it powers a lot of other L2 and has a vibrant ecosystem. Several NFTs, crypto projects, and DApps are running on Ethereum.

The native token of Ethereum is Ether, with a market cap of $200,068,354,228.

Utility. The use cases of Ether include:

- Means of payment

- Settling of transaction and deployment fees

- Investment purposes

Incentives. Ethereum rewards those who stake ETH with more ETH. Anyone who stakes up to 32 ETH in the Ethereum protocol also has the power to become a validator.

Supply. Although it has no maximum supply, its total supply is 120,482,198. The total supply is currently in circulation. A new Ether will be minted through the PoS mechanism.

Distribution. This was the initial distribution of Ether:

- 16.7% - early contributors

- 83.3% - crowdsale

Governance Tokens in DeFi Protocols

DeFi protocols coordinate their community through on-chain agreements. They reach these on-chain agreements with the tokens. With the setting of blockchain, the main community behind any protocol is its DAO. As DAOs are on-chain organizations, they also need tokens to vote on-chain.

In tokenomics, the relevance of a token in terms of governance is a crucial aspect of tokenomics. How many tokens can a member have before joining the decision-making process? Will the members with more tokens have more voting power?

The importance of a token is beyond its native use cases; governance purposes are equally vital. For example, Aave has a DAO where it discusses its communal issues. Their governance token is AAVE.

Final Thoughts

Tokenomics remains a vital aspect of research before investors bag any token. Similarly, an NFT and crypto project must design befitting tokenomics to thrive. Nowadays, tokenomics is not necessarily enough.

There must be proof of how the designs on the paper correlate with the smart contract terms. Double-check if a notable smart contracts auditor confirms the tokenomics design and considers it safe for investors.

FAQ

What is tokenomics?

Tokenomics is the design of a token's issuance, distribution, and structural management.

Why is tokenomics important in cryptocurrency?

Tokenomics is important in cryptocurrency because if the design of a token is flawed, it will bite the dust eventually.

What is tokenomics in NFT?

Tokenomics in NFT means the structure behind the demand and supply of an NFT.

What is a tokenomics example?

Ether, a project with a market cap of $199,438,083,134, is an example of a project with solid tokenomics. Its initial allocation was 16.7% for the foundation and 83.3% for the crowdsale. It also has a total supply of 1,000,000,000 ETH and a supply schedule of 25,000,000 ETH over time.